The Caribbean is a region of contrasts, where idyllic landscapes coexist with deep economic challenges. Perhaps the biggest of these challenges is the high public debt that stands as a persistent obstacle to sustainable growth and prosperity. While several Caribbean nations have made strides toward economic stability, others remain trapped under the weight of soaring debt burdens. While the reasons vary, natural disasters, small and undiversified economies, and high dependency on tourism, the outcome remains the same, a squeeze on the average person and fiscal troubles. In today’s video, we delve into the 10 most indebted Caribbean countries, highlighting the extent of their fiscal challenges and the ripple effects on their citizens’ lives.

For decades, many Caribbean nations have grappled with unsustainable borrowing levels, with levels of public debt often exceeding 60% of GDP in many cases. Not only will we list the top 10 most indebted Caribbean countries but also take a look into why high debt is so bad and what the future holds.

So join Caribbean Focus as we highlight the 10 most indebted Caribbean countries as of the end of 2024.

How much Debt is too much Debt?

But before we get started, let’s look briefly at how we compare debt. Debt between countries is typically measured by using a debt-to-GDP ratio, which compares a nation’s total debt to its gross domestic product (GDP). This metric is widely used because it provides a clear and standardized measure of a country’s debt relative to the size of its economy, allowing for comparisons across nations with vastly different economic scales.

A high debt-to-GDP ratio is often viewed as a red flag because it indicates that a country’s debt exceeds its economic output, raising concerns about its ability to manage or repay that debt without compromising growth or essential services. Not only that, but high debt can erode investor confidence, increase borrowing costs, and reduce fiscal flexibility, i.e. a government’s ability to pay for essential services, leaving nations vulnerable to financial crises or austerity.

While debt-to-GDP ratios vary widely, for context, Japan has the highest ratio at over 260%, the United States stands at around 120%, and Germany, known for its fiscal prudence, maintains a ratio of roughly 65%. All data is taken from the latest IMF values.

10) Belize – 62.3% of GDP or US$ 2.1 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 2.1 billion |

| Debt-to-GDP ratio(%) | 62.3% |

So who starts our number 10 spot? With a debt-to-GDP ratio of 66.8 percent, we have Belize getting us out of the starting block with a total of US$ 2.1 billion in public debt. Belize has faced a challenging journey with its debt-to-GDP ratio, which has fluctuated significantly over the past decade.

At its peak in 2020, Belize’s debt-to-GDP ratio soared to approximately 103%, driven by the twin crises of the COVID-19 pandemic and Hurricane Eta, which devastated key sectors like tourism and agriculture. However, in recent years, Belize has taken measures to address its debt burden, namely through the restructuring of its “Superbond”. In November 2021, the Government of Belize repurchased USD 553 million, a quarter of the country’s total public debt, from bondholders at a 45 percent discount through a “Blue Loan” arranged by The Nature Conservancy, drastically reducing its debt by about 12 percent. Since then the country’s debt continues to drop and is expected to do so into 2025.

9) Jamaica – 67.9% of GDP or US$ 14.7 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 14.7 billion |

| Debt-to-GDP ratio(%) | 67.9% |

Next up on our list, we come to the economic giant and renowned country that is Jamaica. Doing much better than other countries on our list, Jamaica’s debt-to-GDP ratio stands at 67.8 per cent, which equates to approximately US$ 14.7 billion in public debt.

Unfortunately, Jamaica has been burden by a high level of debt for decades, for example, back in 2012, the country saw its debt peak at 143.9 percent of GDP. Recognizing the unsustainable nature of its debt, the government embarked on an ambitious reform program, supported by the IMF focused on fiscal consolidation, structural reforms, and debt restructuring leading to the reduction of public debt by over 60 percentage points.

However, challenges remain: the country continues to face high poverty rates, vulnerability to climate change, and a reliance on tourism and commodity exports. All this does not help a country that has been among the slowest growing economies in the Latin America and Caribbean region with persistently low productivity growth.

8) Antigua and Barbuda – 69.6% of GDP or US$ 1.7 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 1.7 billion |

| Debt-to-GDP ratio(%) | 69.6% |

Our next country is much smaller than the aforementioned Jamacia but does not make their debt-to-GDP ratio any less staggering. With a debt-to-GDP ratio of 69.6 percent or US$ 1.7 billion in debt, Antigua and Barbuda comes in at our number 8 slot. Antigua and Barbuda’s debt-to-GDP while high, has remained fairly consistent over the decades, showing debt is not necessarily always bad.

While the country’s debt-to-GDP ratio peaked at the height of the COVID-19 pandemic, the country’s ratio only just hit 100 percent and has been falling ever since, with a 30 percentage point reduction in just an impressive 4 years. However, this does not mean it’s smooth sailing. The country’s relatively small size makes it vulnerable to external shocks, not to mention the common challenges of climate disasters and an overreliance on tourism most Caribbean countries face.

7) St. Lucia – 73.8% of GDP or US$ 1.97 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 1.97 billion |

| Debt-to-GDP ratio(%) | 73.8% |

With a debt-to-GDP ratio of 73.8 percent or US$ 1.97 billion in debt, we have the home of the pitons, St. Lucia comes in at our number 7 slot. Saint Lucia also becomes the first country on our list where their debt is trending in the wrong direction, rising steadily over the years.

Before the COVID-19 pandemic, Saint Lucia’s debt-to-GDP ratio was around 60%, a manageable level given its developing economy. However, the pandemic dealt a severe blow to its tourism-dependent economy, causing a sharp contraction in GDP and a surge in public borrowing to address health and social needs. In 2020, the debt-to-GDP ratio peaked at 95 percent and even though this value has fallen, concerns still abound about the country’s debt sustainability.

6) Grenada – 75.3% of GDP or US$ 1.1 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 1.1 billion |

| Debt-to-GDP ratio(%) | 75.3% |

Moving on up the list, we come to our next country with a debt-to-GDP ratio of 75.3 percent or US$ 1.1 billion in debt, that’s right, it’s Grenada in our number 7 slot. While 75 percent seems high, and it is, Grenada has demonstrated remarkable progress in reducing its debt-to-GDP ratio over the last decade from its peak of 105 percent in 2013.

Grenada embarked on an IMF-supported reform program in 2014, which included fiscal consolidation, debt restructuring, and economic diversification efforts. However, the country remains vulnerable to external shocks, such as natural disasters like Hurricane Beryl. The damage cause by Hurricane Beryl led Grenada to become the first country in the world to activate its “hurricane clause,” which suspend repayment of its next two debt payments for a few months so funds could be focuse on recovery.

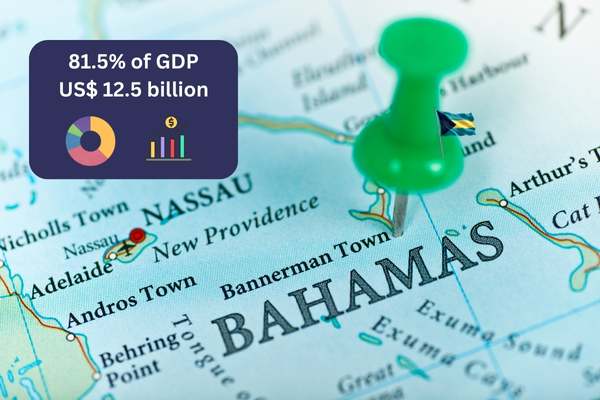

5) The Bahamas – 81.5% of GDP or US$ 12.5 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 12.5 billion |

| Debt-to-GDP ratio(%) | 81.5% |

As we break into the top 5 most indebted countries in the Caribbean, we come to another giant economy in the region in the North, the Bahamas. The Bahamas takes it up a notch with a debt-to-GDP ratio of 81.5 percent, equating to about US $12.5 billion in debt. While not at its highest point in history, before the pandemic the country was on a dangerously upward trajectory, with the country’s debt peaking at 99.7 percent during the height of the pandemic.

However, as the country’s debt continues to decline, the Bahamas remains highly vulnerable to external shocks like Hurricane Dorian which causes a massive surge in expenditure to rebuild. Looking ahead, the country’s ability to reduce its debt burden will depend on tourism growth and improved borrowing costs.

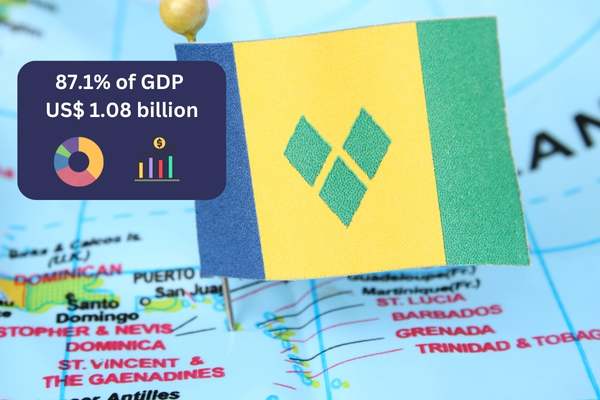

4) Saint Vincent and the Grenadines – 87.1% of GDP or US$ 1.08 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 1.08 billion |

| Debt-to-GDP ratio(%) | 87.1% |

In our number 4 slot, we have another country trending in the wrong direction when it comes to debt-to-GDP, St. Vincent and the Grenadines. With a debt-to-GDP ratio of 87.1 per cent, St. Vincent and the Grenadines hold about US$ 1.08 billion in public debt marking 2024 as the most debt owned by the country in its history.

The reason for this growth in debt can be blame on the deterioration of the country’s primary fiscal balance, cause by the pandemic and the subsequent volcanic eruption in April 2021 which was compounde by Hurricane Beryl just last year in 2024 causing more than US $300 million in damages. The good news, however, is that the country is projecte to begin decreasing its debt by this year 2025.

3) Suriname – 90.3% of GDP or US$ 4.48 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 4.48 billion |

| Debt-to-GDP ratio(%) | 90.3% |

We now come to the region’s most indebted countries, as we come to our number 3 spot taken by Suriname. Suriname becomes our first country with a debt-to-GDP ratio above 90 per cent, with its debt equating to a whopping US$ 4.48 billion or 90.7 per cent of GDP. Suriname has struggled with a volatile debt-to-GDP ratio in recent years, driven by a combination of economic mismanagement, external shocks, and the decline of key industries.

By 2020, the debt-to-GDP ratio had skyrocketed to nearly 150%, one of the highest in the region at the time, due mainly to falling oil and gold revenues, a depreciating currency, and the fiscal pressures of the COVID-19 pandemic. As a result, Suriname entered into a debt restructuring agreement with international creditors and sought support from the International Monetary Fund (IMF) to stabilize its economy. This has led the country to see a downward trajectory of its debt and with the discovery of substantial offshore oil reserves, the country is hoping to see a similar boom to its neighbour Guyana.

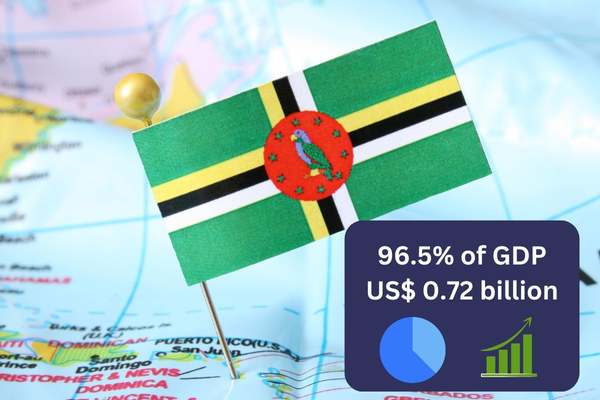

2) Dominica – 96.5% of GDP or US$ 0.72 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 0.72 billion |

| Debt-to-GDP ratio(%) | 96.5% |

Coming in at our runner-up spot, we have another tiny country with a small economy, Dominica. With a debt-to-GDP ratio of 96.5 per cent, that number may seem like a lot, but with a GDP of only US$ 750 million, its total debt is far smaller at just US$ 724 million. Dominica has a history of high debt, hovering above 70 per cent for almost a decade.

Dominica’s longtime challenge with its debt-to-GDP ratio reflects the vulnerabilities of its small economy to external shocks and natural disasters. The country’s debt-to-GDP ratio had slowed and began to trend downwards in 2015, but with the devastation caused by Tropical Storm Erika, was one of the deadliest and most destructive natural disasters in Dominica, the country has seen a gradual increase in its debt obligations.

1) Barbados – 103.2% of GDP or US$ 0.72 billion

| Metric | Value |

|---|---|

| Debt-to-GDP | US$ 0.72 billion |

| Debt-to-GDP ratio(%) | 103.2% |

And in the number 1 spot, we have the unenviable title of the most indebted Caribbean country with a debt-to-GDP ratio of 103 percent. Barbados comes in as the most indebted country in the region owing US$ 8.42 billion to external creditors. The history of Barbados’ debt is not new, since the global financial crisis back in 2008, the country had steadily seen its debt increase year on year, peaking at a whopping 142.8 per cent in 2017. This made it one of the most indebted countries in the world at the time only behind Japan caused by years of fiscal deficits, low economic growth, and unsustainable borrowing.

In response, a new government implemented an ambitious debt restructuring program under the Barbados Economic Recovery and Transformation (BERT) plan, supported by the International Monetary Fund (IMF). These efforts, combined with fiscal reforms and economic adjustments, reduced the debt-to-GDP ratio to approximately 125% by 2023. However, the COVID-19 pandemic reversed some gains, as tourism revenues collapsed and public spending increased to address the crisis.

The future for the country however seems bright. Since 2020, the country has consistently decreassed its public debt year on year and the country is set to drop below the 100 percent figure this year 2025, for the first time since 2011. Looking ahead, Barbados is committed to further reducing its debt-to-GDP ratio to 60% by the fiscal year 2035/36 in accordance with the Barbados Economic Recovery and Transformation (BERT) plan. With prudent fiscal management and strong economic growth, do not let the high debt fool you, the country is set to have a bridge future.

Navigating a Path to Fiscal Sustainability

In short, the high debt-to-GDP ratios of many Caribbean countries highlight the region’s vulnerability to external shocks, natural disasters, and economic reliance on tourism. While the majority of Caribbean countries are trending in the right direction, to ensure long-term stability, nations must go beyond sound fiscal policy to include economic diversification, climate resilience, and fiscal hedging.

Nevertheless, the resilience of the region offers hope that with sustained efforts, the Caribbean can achieve a more secure and sustainable economic future. By continuing to prioritize prudent fiscal management and sustainable development, the Caribbean can lay the foundation for a more secure and prosperous future.